Founders Life and Health Blog |

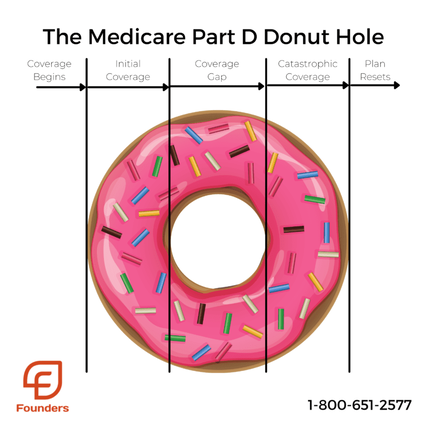

Many of my clients are talking to me right now about the donut hole, what it is, and how it affects their prescription drug coverage. So in my helpful article, I will cover the main points of this confusing topic and hopefully, shed some light on it. So before we delve into details, let’s start with the mini takeaway. What is a donut hole? The coverage gap or donut hole refers to the way a person needs to pay for prescription drug coverage. A specified amount is paid and once met, their plan takes over the funding. However, when the plan has paid up to a specified limit, it is commonly known as the donut hole. Ok with the brief answer in mind, let’s start by finding out an overview of the doughnut hole so you can more easily understand its impact. Donut hole. An overviewSo the easiest way I think to help my clients get to grips with this bewildering topic is when we understand the donut hole refers essentially to the ‘hole’ in your drug coverage. This is where your carrier won’t be contributing as much to your prescriptions as they have previously. Another way of looking at it is a temporary limit on what the drug plan will cover for drugs. For that reason, it’s worth understanding how this lack of coverage in your prescription contributions will affect you. This way you can be fully prepared for the outcome. “your carrier won’t be contributing as much for your prescriptions as they have previously.”  Four stages of prescription coverageI find my clients have a better understanding of this baffling topic by understanding the four stages of your prescription drug coverage. But before we look into those, it’s worth understanding that depending on your plan, there may or may not be a stage 1 phase. Some plans don’t charge a deductible. You pay co-payments or coinsurance for your drugs after you pay the deductible. So for example those of you who are on a Medicare Advantage Plan, it could be that your deductible is zero. “depending on your plan, there may or may not be a stage 1 phase.” Stage one – Deductible phaseStage one of your plan can be fairly easily described as a deductible phase. Simply put, most Medicare part D plans have a deductible or a certain amount of money before the plan kicks in. This means you’ll pay 100% of your prescription costs until you reach your deductible. This can vary enormously depending on your plan. For example, some of my clients might have anything from $150 through to $1000 prescription drug coverage. “This means you’ll pay 100% of your prescription costs until you reach your deductible.” Stage two – Initial coverageIn this stage, the best way to explain it is if you think of it as the part of your prescription coverage that both you and your provider contribute to. In simple terms, you will share the cost with your provider, through the payment of deductibles and coinsurance. The amount at which this stage ends will vary year upon year, so you will need to check your plan thoroughly to find out your responsibility. For example, It might be 100% or 80/20 so make sure you check it out for each time period of your cover. “In simple terms, you will share the cost with your provider” Ok so with this in mind, we’ve now reached stage three, the donut hole!  Stage three – The donut holeIn a nutshell, as we saw previously, the donut hole is the point at which the deductible limit has been reached, your plan will take over in terms of funding your prescription coverage. It’s essentially a ‘coverage’ gap in your plan. As we saw earlier, not everyone will enter a coverage gap. Also, people with Medicare who get extra help paying Part D costs won’t enter the coverage gap. The donut hole begins after you and your drug plan have spent a certain amount for covered drugs. The donut hole itself refers to the point at which that funding has reached its specified limit. So for instance in 2021, according to Medicare, once you have reached $4,130 on covered drugs, you will reach the donut hole. This is often referred to as ‘catastrophic coverage’ “The donut hole itself refers to the point at which that funding has reached its specified limit.” Stage four – Catastrophic coverageDoes the donut hole go away? Often my clients wonder if the donut hole ever goes away! However, in my experience unfortunately it doesn’t go away. You may have heard of ‘closing the donut hole’. So what does this mean? What is meant in simple terms, is that your responsibility lessens. For instance, one of my clients may be paying 25% of their prescription costs when in the donut hole. Once you’ve reached your covered limit, your carrier will pick back up where he left off. As do many of us,( including me!) learn more by a visual representation, I hope this helpful graphic makes it a little simpler to understand!  “Once you hit stage 4, it will be anything over $6350.” Ok so now we’ve looked at the four stages so we can better understand what is meant by the donut hole, you might be wondering how to navigate this tricky stage? Read on to find out my expert recommendations. What should I do when I hit the donut hole?So as I said previously, it’s all about being fully prepared for stage 4. Also, it will totally depend on the kind of plan you’ve taken out. It could be a Supplement, Advantage Plan, or Original Medicare. The whole process can be vastly confusing, so reach out for help in deciphering these complex plans. This way you won’t get any nasty surprises when you finally hit that donut hole. So here are my top tips for what to do when you reach the donut hole.

“The whole process can be vastly confusing, so reach out for help in deciphering these complex plans.” And finally…So I hope my helpful article has helped you to understand more about the tricky donut hole phase of your prescription coverage plan. If you would like to get in touch, I would love to help you discover more and guide you through the process. Or if you have any more questions, maybe take a look at my accompanying YouTube video or drop me a message. If you have any ideas about any further topics for blogs and videos please get in touch. About the AuthorHello! I’m Jo Hutchison and I’m the owner of Founders Life & Health. I’m a proud baseball mom, lover of live music and all things potato.. My husband and I have two great boys and two lazy hound dogs. My boys play a LOT of baseball so when I’m not helping my clients we can almost always be found on a baseball field somewhere in the Midwest. I’m a member of NAIFA (National Association of Insurance and Financial Advisors) and a member of NAHU (National Association of Health Underwriters). I spend a good deal of my time working on educational outlets and working on healthcare policy change to help bring comprehensive and AFFORDABLE coverage to everyone. Nothing makes me happier than sharing the tidbits of knowledge that I know about the Medicare and health insurance world so people can make the most informed decisions about what plans they need. The most important thing that I have learned through the years in this business is that each client has very different needs. Our goal is to listen to you, assess your needs, and use our experience and knowledge to help you make informed decisions about your health care coverage. We are an independent brokerage so we advocate for our clients, not the insurance companies.

0 Comments

Leave a Reply. |

Contact Us(800) 651-2577 Archives

October 2023

Categories |

RSS Feed

RSS Feed

|

We are based in beautiful St Louis Missouri but we are licensed in most states throughout the U.S. |

Navigation |

Connect With UsShare This Page |

Contact Us |

Location |