Founders Life and Health Blog |

How much does Medicare cost?Is Medicare free? That is a great question and it’s not as easy to answer as you would think. The answer is, as you would expect, not quite so easy to answer. For some parts, yes, but for some parts, no. Free MedicareFirst thing’s first though, you will never hear the word free used all by itself from any legitimate Medicare representative. Medicare does not like the word free when it stands all by itself. You will, however, hear the words “no charge”, “zero premium” or “premium free” with the word premium in front of it, but never just the word “free”. Medicare does not like the word free all by itself. Decoding the jargon of Medicare honestly is half the battle.  So if it’s not free, then what does it cost? There’s a couple of different options to look at. You’ll want to start with, if we’re looking at:

Original MedicareIf you are looking at just Original Medicare Parts A and B, here’s what you can expect to pay for. Medicare Part A costFor Part A, which is your just hospital coverage, that is what they’re going to call “premium free”. It will be “premium free” if:

If you are under 65, you can get premium free Part A if

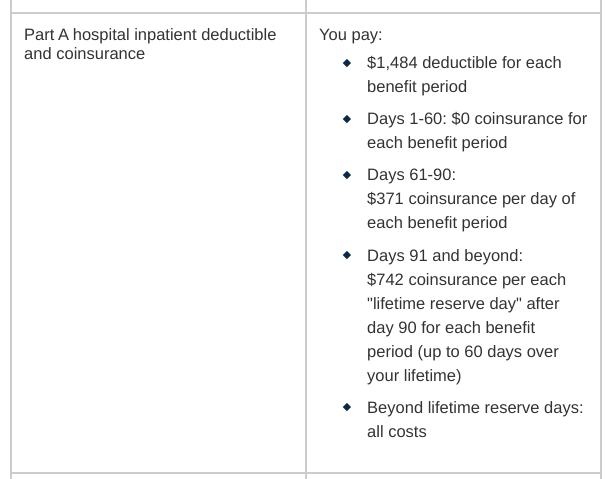

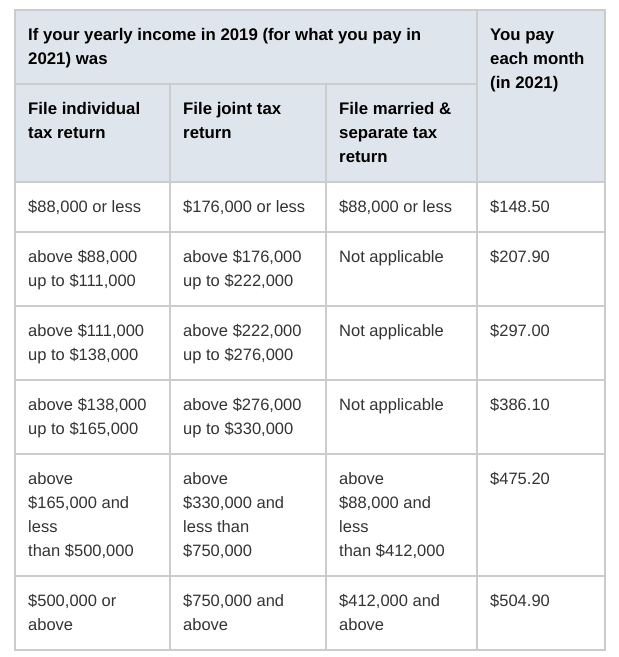

One extra thing to think about, if you don’t qualify for premium free Part A, you can buy Part A. People who buy Part A will pay a premium of either $259 or $471 each month, that’s just for this year, 2021, depending on how long they or their spouse worked and paid Medicare taxes. Keep in mind, if you’re reading and it’s no longer 2021, some of those amounts may have changed.  Medicare Part A deductible 2021Okay, here’s where the money comes in for Part A. The deductible for Part A is $1,484, that is for the year 2021. So keep in mind again, if you’re reading this and it’s no longer 2021, that number may have changed. Medicare part A hospital coverageThe other part that’s going to cost you money for Part A is if you have a hospital stay past 61 days, you can expect to pay all of these charges here. They’re going to piece it out by how long you’ve been in the hospital. Here is the current chart for 2021:  Cost of Medicare Part BMoving on to Part B of Original Medicare, you are going to pay two things for your Part B. You’re going to pay your monthly premium and you will pay the deductible.  So as you can see here, your part B premium is based on your income. And that is a monthly cost. Medicare part B premium 2021Two other costs to keep in mind for Original Medicare Part B, you will have an annual deductible of $203. That’s probably going to change if you’re seeing this later than 2021. And the other thing, which is the really big piece of the puzzle is that you are going to have a 20% co-insurance for anything else that you have done. So if you have a big surgery or you have treatments and you’re getting charged for those, you are going to be responsible for 20% of the cost of all of that, which is why people usually look into either a Medicare Advantage Plan or a Medicare Supplement.  Medicare Supplement PlansIf you have a Medicare Supplement, what can you expect to pay for? The first thing you can expect to pay for on a Medicare Supplement is going to be your monthly premium. The premium will be different based on several different factors. It will be based on the company that you choose. It will be based on the letter type plan that you choose. It will be based on the zip code that you live in. And it will also be based on if you applied for a Medicare Supplement when you were not in your initial enrollment period, and you had to go through underwriting, you will probably pay a higher premium. Next thing you can expect to pay for is going to be your annual deductible, and that’s that $203 annual deductible, unless, and you know in Medicare it’s so fun because there’s always an unless or a in case of or in other situations. Unless you were eligible for Medicare before January 1st, 2020, then you would be eligible for a Plan F and some of the Plan Fs would cover the annual deductible, so you would not have to pay for that. Next, depending on your letter plan, if you decide to go with a letter plan where you may have additional costs, then you may have what they call excess charges. Those could be some additional things that would pop up on your plan. Typically, they are not going to come up in a Plan G. You could see excess charges in a Plan N, but when you get to the point that you are exploring a Medicare Supplement, talk to your Medicare advisor and get all of the particulars so that you’re not hit with any surprises. Medicare Part D premium Last, but certainly not least, is your prescription drug coverage. So if you have a Medicare Supplement, you are going to need prescription coverage in addition to your Medicare Supplement. So that will be a separate plan outside of the supplement but it will absolutely cost you more money. And that is a whole other ball of wax that you can get into with your Medicare adviser talking about the donut hole and what you’re going to expect to pay before you meet the middle of the donut hole.  Medicare Advantage PlansYour third option, of course, is going to be if you have a Medicare Advantage Plan. So what are going to be the cost associated with that? First and foremost is going to be the monthly premium. On a lot of the Medicare Advantage Plans that I’ve worked with, they might be “zero” cost or “zero premium”, or they’re going to be a much smaller amount, but it’s going to depend again on the area that you’re in, the plans that are available in that area. So you’re going to have to talk to the Medicare advisor that you work with to find out what the plans that are available and what those costs would be. Some Medicare Advantage Plans will cover your Part B Premium Original Medicare. Again, you’ll want to check with your plan and check with your advisor and find out if that is something that is covered or not covered under your Medicare Advantage Plan. Typically, on a Medicare Advantage Plan, you are going to have a larger annual deductible. Something you’ll want to pay particular attention to on your Medicare Advantage Plan is what the annual deductible will be. Medicare Maximum Out of PocketWhen you’re looking at these plans there is something that you should pay attention to call the “Maximum Out-Of-Pocket” or “MOOP”. Every plan on a Medicare Advantage is going to show you very specifically what the maximum amount every year that you will pay will be. That’s really going to be important for you to pay attention to because that is going to cover all of your deductibles, your co-payments, your co-insurance, everything is going to be wrapped up in that. And then once you hit that maximum out of pocket, then there won’t be any more costs up to you after that to you. More often on a Medicare Advantage Plan, you are going to see co-payments at your doctor’s visits and at your specialist visits. So when you’re looking at your plan, again, you want to take a look at that and see what those co-payments are going to be. Medicare Advantage Plan NetworksBONUS HINT #1 The thing you’re going to want to pay the most attention to is your network. Because a Medicare Advantage Plan is going to keep you in a network. You are going to have to see certain doctors in that network, you’re going to have to have referrals for certain specialists in that network, depending on the type of plan you have. So if you end up out of network for any services, your cost could be a lot higher and that maximum out-of-pocket is not going to apply anymore, there’s going to be different numbers affiliated with that. You want to make sure that you stay in network if you’re going to be doing any of those services. BONUS HINT #2 Another really helpful tool that you can use is on the medicare.gov website. They have a really handy tool where you can put in any procedure that you’re going to have, and it will tell you what the Medicare reimbursement cost is for that. You will know in advance what the cost of that procedure will be. And then you can apply that depending on what you have, whether you have Original Medicare or Medicare Supplement or an Advantage Plan, you can use that information to kind of plug into your plan and see where you’re going to end up at. BONUS HINT #3 If you need help paying for your Medicare, there are lots of resources out there that can help with that. I’m going to put another link down below that will link to the medicare.gov site that will give you additional information about resources that you can use to help pay for your Medicare. Hopefully that was helpful. If you are getting ready to turn 65, check out my video on if you’re turning 65, a checklist for all the things to think about. And if you have questions, as always, feel free to reach out. About the AuthorHello! I’m Jo Hutchison and I’m the owner of Founders Life & Health. I’m a proud baseball mom, lover of live music and all things potato.. My husband and I have two great boys and two lazy hound dogs. My boys play a LOT of baseball so when I’m not helping my clients we can almost always be found on a baseball field somewhere in the Midwest. Nothing makes me happier than sharing the tidbits of knowledge that I know about the Medicare and health insurance world so people can make the most informed decisions about what plans they need. The most important thing that I have learned through the years in this business is that each client has very different needs. Our goal is to listen to you, assess your needs, and use our experience and knowledge to help you make informed decisions about your health care coverage. We are an independent brokerage so we advocate for our clients, not the insurance companies.

0 Comments

Leave a Reply. |

Contact Us(800) 651-2577 Archives

October 2023

Categories |

RSS Feed

RSS Feed

|

We are based in beautiful St Louis Missouri but we are licensed in most states throughout the U.S. |

Navigation |

Connect With UsShare This Page |

Contact Us |

Location |